Natural disasters can be devastating, causing significant damage to homes and property. Understanding how property insurance covers these events is crucial for ensuring you have the protection you need. Here’s a comprehensive look at how property insurance addresses natural disasters and what you should consider to safeguard your property effectively.

1. Types of Natural Disasters Covered

Property insurance typically covers a range of natural disasters, but the extent of coverage can vary depending on the type of disaster and the specifics of your policy. Common natural disasters and their coverage include:

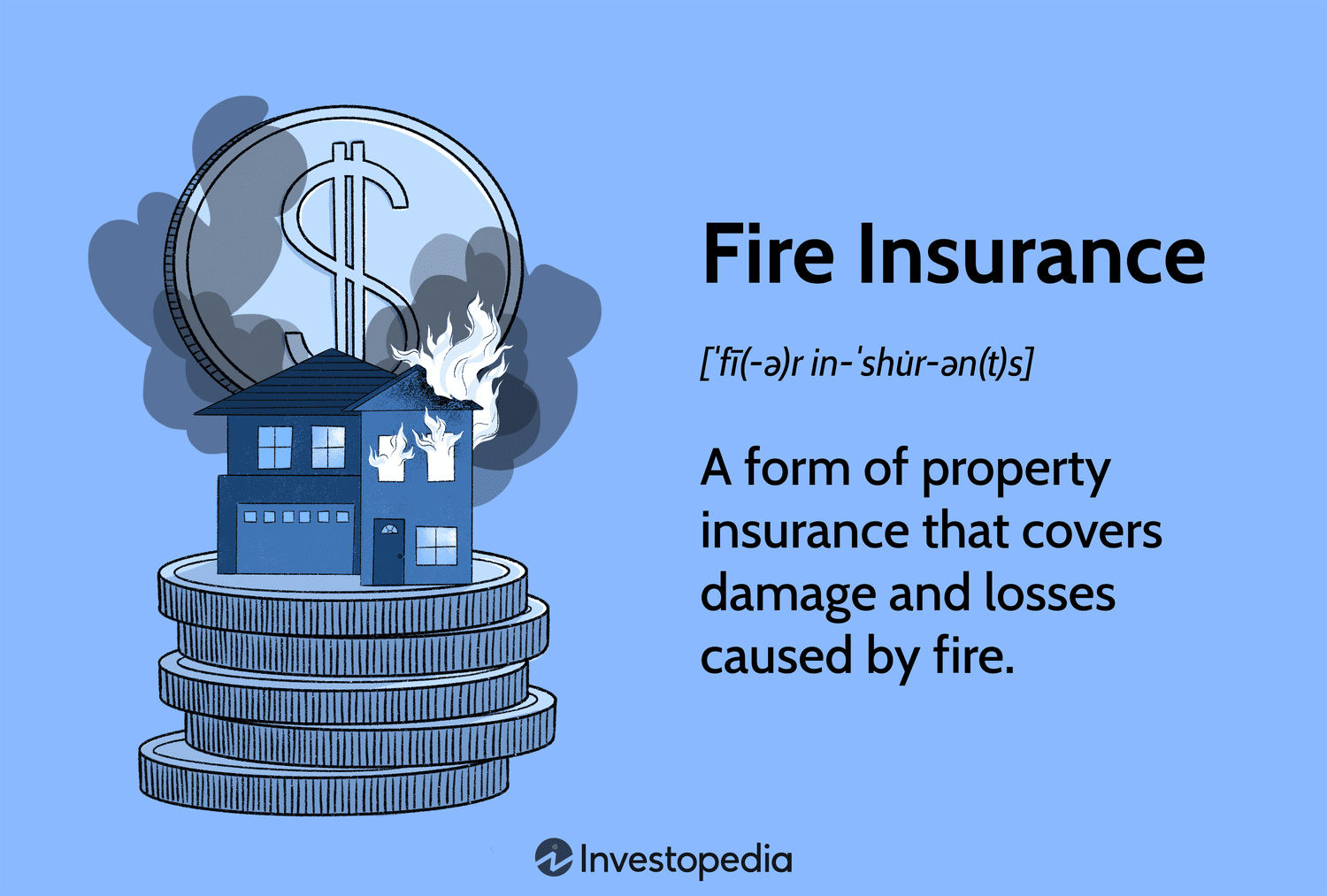

- Fire: Standard property insurance policies usually cover damage caused by fire, including wildfires. Coverage includes repairs to the structure, replacement of damaged belongings, and additional living expenses if you’re temporarily displaced.

- Windstorm and Hail: Most property insurance policies cover damage from windstorms and hail. This includes damage to the roof, siding, windows, and other parts of your home. However, coverage for wind damage might be limited or require a separate endorsement in high-risk areas.

- Lightning: Damage from lightning strikes, such as electrical surges and fires, is generally covered under standard property insurance policies. This includes repairs and replacement of damaged electrical systems and appliances.

2. Flood and Earthquake Coverage

Floods and earthquakes are significant natural disasters that often require additional coverage:

- Floods: Standard property insurance policies do not cover flood damage. To protect against floods, you need to purchase separate flood insurance through the National Flood Insurance Program (NFIP) or a private insurer. Flood insurance covers damage to the structure of your home and personal belongings, but it’s essential to understand the specific terms and limits of your policy.

- Earthquakes: Earthquake damage is typically not covered by standard property insurance. If you live in an area prone to earthquakes, you should consider purchasing earthquake insurance. This specialized coverage addresses damage to your home and belongings caused by seismic activity and often includes additional living expenses if your home becomes uninhabitable.

3. Policy Exclusions and Limitations

It’s important to be aware of exclusions and limitations in your property insurance policy:

- Named Perils: Property insurance policies often cover damage from named perils specified in the policy. If a natural disaster is not listed as a covered peril, it may not be covered. Carefully review your policy to understand which natural disasters are included.

- Deductibles: Different types of natural disasters may have separate deductibles. For example, windstorm damage might have a higher deductible compared to other types of damage. Review the deductible amounts associated with each peril to prepare for potential out-of-pocket costs.

- Policy Limits: Coverage limits dictate the maximum amount your insurance will pay for damages. Ensure that your coverage limits are sufficient to repair or replace your property in the event of a significant disaster. Consider adjusting your limits based on the value of your home and belongings.

4. Steps to Ensure Adequate Coverage

To ensure you have the right protection for natural disasters:

- Review Your Policy: Regularly review your property insurance policy to understand your coverage and identify any gaps. Make sure you have adequate coverage for common natural disasters in your area.

- Consider Endorsements: Add endorsements or riders to your policy to cover specific risks not included in your standard policy. For example, you might add coverage for windstorms or earthquake damage if you live in a high-risk area.

- Assess Your Risk: Evaluate the natural disaster risks specific to your location. Flood-prone areas, earthquake zones, and regions susceptible to wildfires may require additional coverage beyond what is offered by standard property insurance.

- Document Your Property: Keep detailed records of your property and belongings, including photos and videos. This documentation can be valuable when filing a claim and ensuring you receive adequate compensation for damaged or lost items.

5. Filing a Claim for Natural Disaster Damage

If you experience damage from a natural disaster:

- Contact Your Insurer: Notify your insurance company as soon as possible to start the claims process. Provide detailed information about the damage and follow the insurer’s instructions for filing a claim.

- Document the Damage: Take photographs and videos of the damage to your property and belongings. This evidence will support your claim and help ensure you receive appropriate compensation.

- Work with Adjusters: An insurance adjuster will assess the damage and determine the payout amount. Cooperate with the adjuster and provide any additional information they request to facilitate a smooth claims process.

Conclusion

Property insurance plays a crucial role in protecting your home and belongings from natural disasters. By understanding the types of coverage available, recognizing policy exclusions and limitations, and taking proactive steps to ensure adequate protection, you can better safeguard your property against the impacts of natural disasters. Regularly reviewing your policy, considering additional coverage options, and documenting your property will help you navigate the complexities of insurance and ensure you are well-prepared in the event of a disaster.