Umbrella insurance is a vital yet often overlooked component of comprehensive risk management. It provides an additional layer of liability coverage beyond the limits of your standard auto, homeowners, or renters insurance policies. While most people understand the basics of primary insurance coverage, umbrella insurance offers extra protection that can safeguard your financial future in ways you might not expect. Here’s why umbrella insurance is crucial for added liability protection.

1. What is Umbrella Insurance?

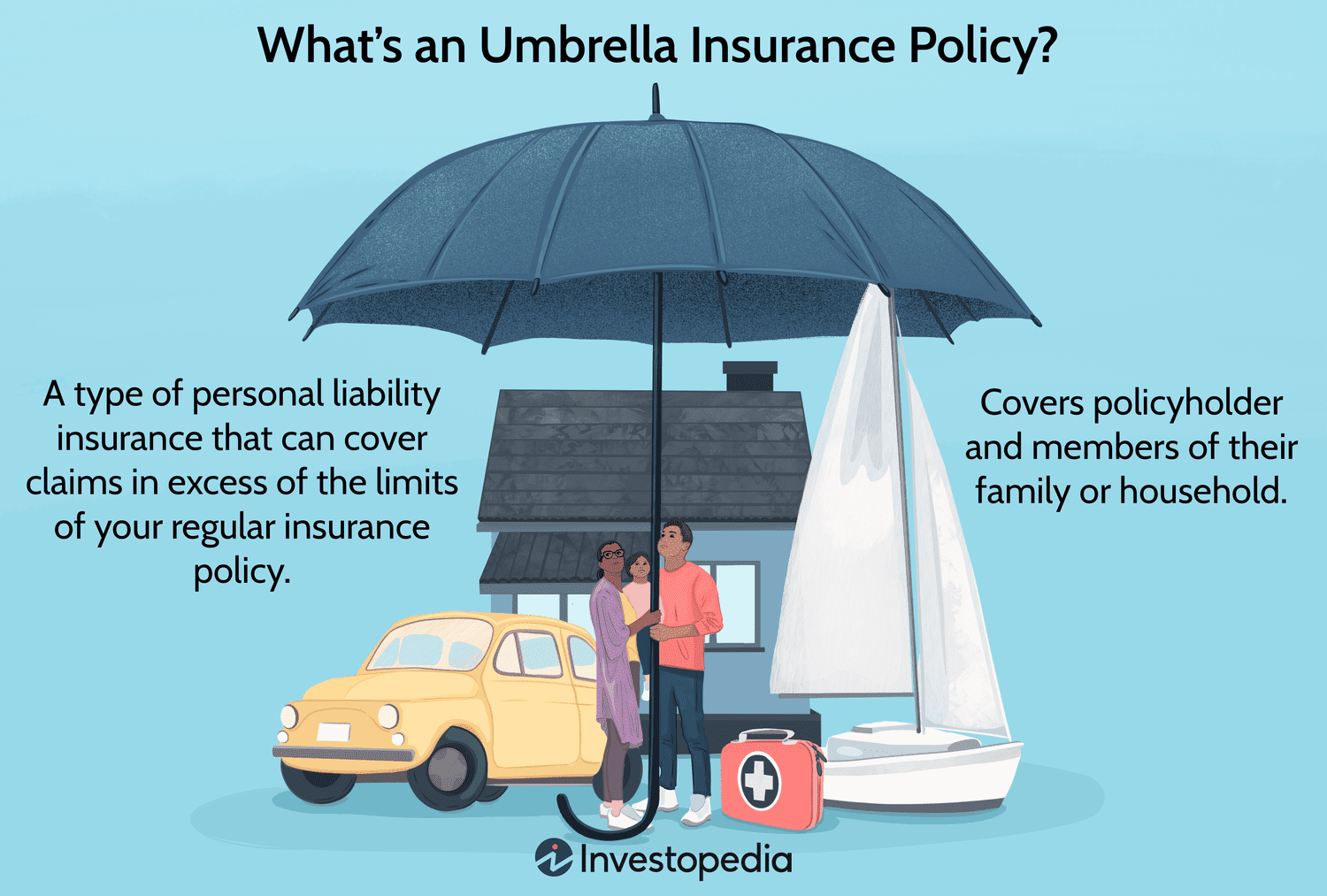

Umbrella insurance is designed to extend the liability coverage provided by your existing insurance policies. It offers a high limit of coverage that kicks in when your primary policies reach their limits. For example, if you are involved in an auto accident and the damages exceed your car insurance’s liability limits, your umbrella policy would cover the additional amount, up to its limit.

2. Protection Against Large Claims

One of the primary benefits of umbrella insurance is its ability to cover large claims that exceed the limits of your primary insurance:

- High-Value Lawsuits: If you are sued for damages or injuries resulting from an accident, medical malpractice, or defamation, the legal costs and settlement amounts can quickly exceed your primary policy limits. Umbrella insurance helps protect your assets by covering these excess costs.

- Personal Liability: Umbrella policies cover personal liability claims not included in your standard policies. This includes incidents such as a guest being injured on your property or accidents involving your pets. The additional coverage can be crucial if the claims are substantial.

3. Affordable Additional Coverage

Umbrella insurance is often more cost-effective than increasing the liability limits on your primary policies:

- Cost Efficiency: Umbrella policies provide a significant amount of coverage at a relatively low cost. While increasing liability limits on your home or auto insurance can be expensive, umbrella insurance offers a higher limit of protection for a fraction of the cost.

- Peace of Mind: For a modest additional premium, you gain substantial extra coverage, which can be a worthwhile investment for peace of mind knowing that you are protected against unexpected large claims.

4. Coverage for a Range of Risks

Umbrella insurance covers a broad spectrum of risks that may not be fully addressed by standard policies:

- Worldwide Coverage: Many umbrella policies offer worldwide coverage, protecting you against claims that arise while traveling abroad. This can be particularly valuable for frequent travelers or expatriates.

- Legal Costs: Umbrella insurance typically covers not only the settlement amounts but also legal defense costs. In the event of a lawsuit, these legal fees can be substantial, and umbrella insurance helps mitigate these expenses.

5. Safeguarding Your Assets

Protecting your financial assets is a primary reason for investing in umbrella insurance:

- Asset Protection: Without adequate liability coverage, a substantial claim could lead to the liquidation of your assets or even personal bankruptcy. Umbrella insurance ensures that your savings, investments, and property remain protected in the event of a large liability claim.

- Future Financial Security: By securing additional liability coverage, you safeguard not only your current assets but also your future earnings and investments. This long-term protection is crucial for maintaining financial stability.

6. When to Consider Umbrella Insurance

Assessing whether umbrella insurance is right for you involves evaluating your risk factors and financial situation:

- High Net Worth: If you have significant assets or high earning potential, umbrella insurance is especially important. It provides an extra layer of protection against claims that could threaten your financial stability.

- Increased Risks: If you have lifestyle factors that increase your risk, such as owning rental properties, hosting frequent social gatherings, or having a teenage driver, umbrella insurance can provide valuable additional protection.

7. How to Obtain Umbrella Insurance

To secure an umbrella insurance policy:

- Consult Your Insurance Agent: Speak with your current insurance agent to discuss your need for umbrella coverage. They can help determine the appropriate amount of coverage based on your existing policies and risk profile.

- Review Policy Terms: Carefully review the terms and conditions of the umbrella policy, including coverage limits, exclusions, and the claims process. Ensure that the policy meets your needs and provides the comprehensive protection you require.

Conclusion

Umbrella insurance is a crucial tool for managing liability risk and protecting your financial future. By extending coverage beyond the limits of your primary insurance policies, it offers an additional layer of protection against large claims and lawsuits. With its affordability, broad coverage, and ability to safeguard your assets, umbrella insurance is a smart investment for ensuring peace of mind and financial security. Assess your risk factors, consult with an insurance professional, and consider adding an umbrella policy to your insurance portfolio to enhance your overall protection.